Transforming MSMEs through E-commerce

Festive Ecommerce Trends | January 2024

The festive

season stretching from Navratri to Diwali & Bhai Dhooj, during the months

of September to November, represents the peak annual business opportunity for

Micro, Small and Medium Enterprises (MSMEs) across consumer-oriented sectors in

India. With discretionary spending rising sharply, these months contribute 35-40%

of annual revenues for MSMEs in retail, consumer goods, apparel, homeware,

handicrafts among others. E-commerce entities accelerate targeted promotions

across this duration, lining up attractive deals, new product launches,

influencer engagement, contests and personalized offers to attract high intent

shoppers.

With the

onslaught of the Covid-19 Pandemic, there has been a drastic change in consumer

buying behavior & patterns in metro cities and this can be seen in the

festive season too. E-commerce platforms have witnessed tremendous growth

during festive sales, with order volumes expanding from US$ 3 billion during

the 2019 season to US$ 5.7 billion in 2022, reflecting a CAGR of 23%.

Categories like fashion, smartphones, consumer electronics and home appliances

see maximum traction. With lockdowns and social distancing measures in place,

more consumers have shifted to online shopping and become more open to

purchasing from small, local businesses.

A continued

shift in consumer and merchant behaviour, matched

with strong investor confidence, has ushered India into its 'Digital Decade'

and set the country on a path to reach a US$ 1 trillion. consumer internet

economy by 2030. Digital services are fast becoming integral to India's 700M+

internet users, which includes 350M digital payment users and 220M online

shoppers. As India undergoes a dramatic boom that will see household

consumption doubling by 2030, digital commerce will invariably become even more

entrenched in Indians' everyday experience*. E- commerce platforms have aided

small enterprises in rapidly expanding from a local customer base to a

nationwide reach.

UPI

Payments which played a pivotal role in financial inclusion also paints a very

promising picture. According to the Ministry of Finance, the total digital

payment transactions volume increased from 2,071 crore in FY 2017-18 to 13,462

crore in FY 2022-23 at a CAGR of 45%**.

Consecutively,

the Open Network for Digital Commerce (ONDC) has also emerged as a game-

changing initiative based on an open-source network aiming to democratize

e-commerce opportunities for micro, small and medium sellers in India. ONDC's

commitment to vernacular interfaces and enhanced logistics through regional

providers maximizes the ability for MSMEs to tap into rising demand from Tier

2/3 markets during seasonal high-spend cycles.

*https://www.bain.com/insights/e-conomy-india-20/23/

**https://pib.gov.in/PressReleasePage.aspx?PRID=1988370

Introduction

This,

combined with accessible digital payment methods like UPI, have made online

purchasing much easier, while simplified taxation norms, like replacing

multiple state taxes with a single GST, have reduced compliance issues for

online sellers by eliminating octroi and tax compliances set by states. Lastly,

the spread of logistical infrastructure network across the different Indian

geographies have made it possible for sellers to reach distant customers.

Planned investments of Rs 22 lakh crores, integrated road-rail connectivity,

UDAN Scheme to expand airport network and Railway Freight Corridors have made

it easy to access pin codes stretching to rural India. Growth of logistics

providers have enabled quick and reliable product deliveries. Platforms like Shiprocket, ElasticRun, and Shyplite that offer access to affordable logistics for

single truckloads have eased fulfillment costs for MSMEs inordinately

increasing sales potential. These factors have cumulatively created a vibrant

ecosystem for ecommerce and boosted online sales across India. This report

intends to show the effect of these factors & trends & how the

frictionless payments, streamlined logistics and favorable policies have shaped

the emerging market dynamics from the point of view of the MSMEs who have tried

to align themselves with the Post Covid World. India SME Forum & FIRST has

actively advocated for MSMEs to embrace digital transformation. This report

will specifically measure the impact of this digital push on MSMEs, with a

focus on those who have adopted e-commerce. Notably, there is a gap in existing

research, and this report aims to fill that void by being the first

comprehensive survey to help MSMEs measure the impact of adopting digital

practices on their businesses.

The

objective of the report is to understand the changes in consumer behavior

especially after COVID-19 that has led to an increase in online buying and with

easy accessibility to internet, we have seen customers from tier-2 and 3 cities

buying more through e-commerce. While initially the major share of online

buyers was restricted to Metros and Tier 1 & 2 cities, today, a

considerable portion also comes from the smaller towns and rural areas. Rapid

adoption beyond metro cities is powering expansion, with e-tailers revealing

that Tier 2 and 3 cities drive nearly 65% of festive revenues, under lining the

vast headroom available as small-town India goes online. This report offers a

comprehensive analysis of the state of e-commerce within the context of peak

festive shopping seasons in India and the contribution of e-commerce towards

the revenues of Micro, Small & Medium Enterprises in India.

The

multifaceted insights provided will serve as a valuable resource for diverse

stakeholders, ranging from marketplace entities to policy regulators and small

business owners. The Government of India's initiative like Digital India and

ONDC, etc., have made the e-commerce ecosystem transparent for both sellers and

buyers. The report also touched on the pain points of online MSMEs and

highlighted the problems related to government and industry

regulators/practitioners. This report aims to conduct a thorough examination of

critical business metrics, encompassing sales revenues, order volumes, sales

growth rates, pricing tiers, and target demographics. The focus is on understanding

emerging shifts in attitudes and online buying intensity from a consumer

perspective during festive sales. Furthermore, an in-depth assessment of seller

experiences and operational capacities, this includes evaluating the efficacy,

trust, and adoption levels of key e-commerce platforms.

The

Methodology

The Forum

for Internet Retailers, Sellers & Traders (FIRST) has been dedicatedly

working towards bringing the practice of adopting Digitalization to the

forefront. In this quest, FIRST has successfully approached and educated around

67,392 MSMEs across India in the last 2 years and continues to do so. These

MSMEs are the members of the India SME Forum and its constituent supporting

organizations and federations.

The survey,

conducted by the India SME Forum aims to comprehensively examine the impact of

e-commerce sales during the festive season and the increasing adoption of the

Direct-to-Consumer (D2C) approach among Micro, Small, and Medium Enterprises

(MSMEs) across India.

To ensure

precision in data collection, a thorough questionnaire was formulated through

extensive deliberation and analysis. The final questionnaire format was

designed to facilitate the gathering of specific data points, thereby

streamlining both qualitative and quantitative analysis. The 67,392 MSMEs

registered under FIRST were approached for data collection for the survey which

commenced with the distribution of survey emails in July 2023. Subsequent

reminders were sent via SMS and telephonic outreach to enhance response rates.

The initial

phase of the survey garnered a total of 34,263 responses. Among these, 32,472

responses were identified as fully complete and comprehensive. However, 1,791

respondents left the survey incomplete and were consequently excluded from

consideration for the purpose of this report. From the pool of 32,472

respondents, the study narrowed its focus to the subset of 22,073 respondents

who reported that they were already actively engaged in online selling. These

respondents were then progressed to Section 2 of the survey for more in-depth

analysis.

Highlights

of the Survey

v 67.9% of the

respondents are currently involved in online selling, while 28% plan to start

soon, highlighting widespread e-commerce participation.

v Over 50% of

sellers reported a significant increase in sales, and 41.7% experienced an 80-

100% expansion of their customer base after adopting e-commerce.

v Trust remained a

cornerstone in the e-commerce ecosystem, with wide customer reach (100%),

company reputation (99%), and a robust seller ecosystem (95%) cited as the top

three reasons driving seller trust in e-commerce websites.

v MSMEs focus on

stocking up inventory, increased advertising, new product launches, and

workforce additions as preparative strategies for the festive season.

v 14,982

respondents reported a 30-40% increase, and 1,795 experienced a boost of over

50% in festive season sales.

v Nearly 80% of

sellers generated their revenues from online and e-commerce sales, with 60%

doubling their sales and 90% registering a minimum 30% YoY increase in online

sales.

v Tier 2 & Tier

3 cities played a significant role, constituting 41.31%, followed by

metropolitan cities at 36.62%.

v Onboarding

difficulties, high returns, lack of seller support, and tax complexities emerge

as major pain points for e-commerce participants.

v Amazon India

leads with 38%, followed by significant preferences for Flipkart, Myntra, and Meesho.

v A noteworthy 57%

of respondents view e-commerce as an ideal Direct-to-Consumer (D2C) platform,

leveraging market reach and trust.

v Digital India,

Telecom and the UPI revolution are primarily responsible for sellers joining e-

commerce platforms.

v 36.37% of

respondents advocate for changes in GST guidelines to simplify compliance

processes.

Digital Transformation Underway

According

to the India Brand Equity Foundation's e-commerce industry report 2023, the

last three years have seen a rise in online shoppers by 125 million and is

expected to increase by another 80 million by 2025*. According to a report by

Deloitte India, as India moves towards becoming the third-largest consumer

market, the country's online retail market size is expected to reach US$ 325

billion by 2030, up from US$ 70 billion in 2022, owing largely to the rapid

expansion of e- commerce in tier-2 and tier-3 cities**.

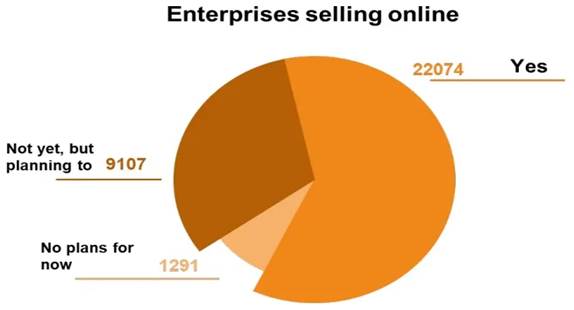

The

survey reported that a majority of the respondents, that is 22073 (67.98%) were

inclined towards online selling, while an additional 9108 (28.05%) of the

respondents express their intentions to venture into online sales.

Surprisingly, 1291 respondents (3.98%) indicated no plans to go online, despite

the active efforts of FIRST (Forum for Internet Retailers, Sellers &

Traders) encouraging MSMEs to establish an online presence, which suggests that

there is still a considerable amount of confusion and prevalent myths in the

market, hindering some individuals from making the transition to online

selling.

The

Open Network for Digital Commerce (ONDC) has also emerged as a game-changing

initiative based on an open-source network aiming to democratize e-commerce

opportunities for micro, small and medium sellers in India. ONDC's commitment

to vernacular interfaces and enhanced logistics through regional providers

maximizes the ability for MSMEs to tap into rising demand from Tier2/3 markets

during seasonal high-spend cycles.

*https://www.ibef.org/industry/ecommerce

**https://www2.deloitte.com/in/en/pages/about-deloitte/articles/future-of-retail-emerging-landscape-of-omni-channel-commerce-in-India.html

From Third Party or No Brands to Brand Owners

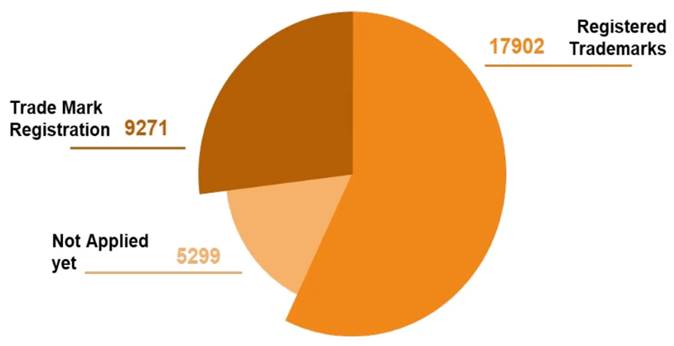

With

the surge in India's e-commerce sector, the survey underscores a growing

awareness among businesses regarding the importance of intellectual property

(IP), particularly trademarks. A substantial 55.13% (17902) of respondents

reveal they have already registered trademarks, with an additional 29% (9271)

currently in the process of doing so. Only 16% (5299) indicate a lack of

trademarks in their portfolio. This demonstrates that 27,173 out of 32,372

respondents are aware about the IPR and its importance in their growing

business.

The

success of these awareness efforts can be attributed to the initiatives

undertaken by the India SME Forum (ISF) & its Centre of IP Research,

Promotion and Facilitation (CIPRPF) which has played a pivotal role in

educating entrepreneurs about trademarks and their significance. This success

is underscored by the impressive 85% success rate of ISF campaigns related to

intellectual property rights (IPR).

This

trend aligns with the broader landscape of intellectual property registrations

in India, which has witnessed a remarkable upswing. According to 2022 data from

the World Intellectual Property Organization (WIPO), India ranks fifth globally

in annual trademark applications and sixth in patent filings, consistently

outpacing global averages. A report by the Organization for Economic

Cooperation and Development or the OECD talks about the rise in risks of

counterfeiting with selling products online through e-commerce platforms. Thus,

as more businesses sell their products online it becomes essential for them to

register for trademarks and protect their intellectual property**. A rise in

e-commerce retail can thus also be correlated to the rise in trademark

registrations.

*https://www.managingip.com/article/2ban50tiglik/4wtigBaskcg/expert-analysis/local-insights/india-a-statistical-analysis-of-trends-in-ip-rights

*https://www.oecd-library.org/sites/2abaae54-onv/index.html?itemid-%2Fcontent%2Fcomponent%2F2abaa054-on

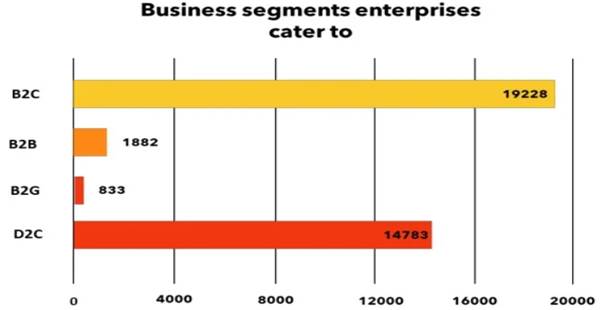

D2C Gains Popularity in India

Among

the 22,073 respondents, a significant majority-19,228 respondents are oriented

towards the B2C segment, showcasing a strong emphasis on direct consumer

engagement. Additionally, 14,783 respondents are actively involved in the D2C

segment, which has experienced heightened popularity, particularly through

e-commerce platforms, in the post-pandemic era. The India SME Forum (ISF) has

actively promoted the D2C model, leveraging success stories from the brands

like SUTA, BLUE TEA and AMRAPALI.

In

terms of other market segments, 1,882 respondents focus on B2B segment and a

smaller yet noteworthy group of 833 respondents engage in B2G segment. It's

important to note that this classification pertains specifically to respondents

who have taken their businesses online, and the numbers could be higher if

offline-mode businesses were also considered. High competition from large

established brands, limited marketing budgets and lack of bargaining power make

it tough for MSMEs to get shelf space at modern trade stores or tie ups with

major distributors. Additionally, small production volumes, inconsistent

quality and inability to offer credit terms or discounts like bigger players

which further restricts MSME retail access. MSMEs also face challenges meeting

diverse state regulations and managing logistics for widespread distribution.

As of July 2023, an impressive 65.42 lakh sellers are registered on GeM, including 8.32 lakh MSMEs. ISF has further

strengthened this initiative by signing a Memorandum of Understanding with GeM, facilitating collaboration to conduct

capacity-building workshops and training programs related to the portal. This

partnership aims to enhance the overall SME ecosystem, while also promoting key

initiatives such as Womaniya, Startup India, National

Livelihoods Mission, and more.

According

to a report by Shiprokcet, the Indian D2C market was

approx. $12 Billion in 2022 with a CAGR of 40%, which is expected to reach

around $60 Billion by 2027. India is expected to be the third largest economy

by 2030 with ~40% of the population living in urban areas; India to have 1.3

billion+ smartphone users and internet users and ~50 million online shoppers by

2030.

D2C

brands are scaling rapidly, these brands are reaching INR 100 Cr milestone in

3-5 years after launch.*

D2C

model leveraging e-commerce is gaining major traction among Indian MSMEs to

boost sales & reach new markets. MSMEs can sidestep traditional retail

channels & distributors while gaining visibility through targeted digital

marketing & enables MSMEs to easily list and sell products without heavy

inventory or warehousing costs. It provides access to millions of potential

buyers & keeps overheads low.

*India

D2C Report 2022 by Shiprocket

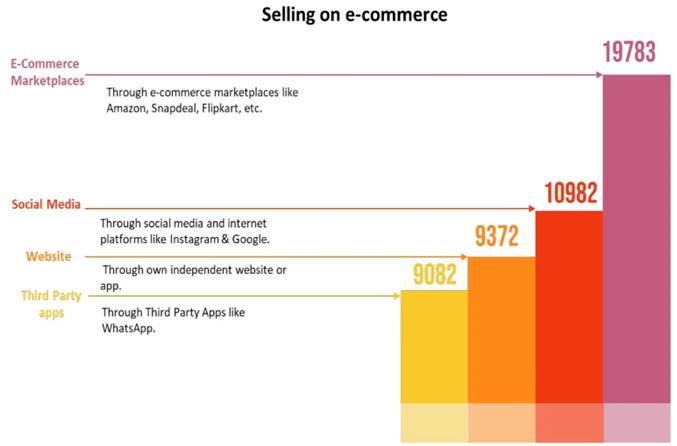

Omni-channel is IN

The

survey revealed that a majority of respondents that is 19,783 engage in selling

their products through various online channels, with a notable presence on

e-commerce platforms such as Amazon, Flipkart, and Snapdeal. Additionally,

10,982 respondents utilize social media platforms like Instagram and Google,

indicating a growing trend and among the respondents, 9,372 also mentioned

selling ontheir own websites or apps, while 9,082

opted for third-party apps like WhatsApp.

India

SME Forum (ISF) has been actively pushing for the establishment of individual

business websites instead of solely relying on e-marketplaces. This strategy is

likened to having one's own shop as opposed to operating within a mall. This

holistic and diversified approach, often referred to as an omnichannel

strategy, enables businesses to engage with customers across various platforms

and channels, thereby enhancing their reach and adaptability in the dynamic

digital landscape.

E-commerce

platforms, especially Amazon, emerged as a predominant choice for online

product sales, attributed to several advantages for businesses. These

advantages encompass a swift selling process, cost reduction, affordable

marketing, extensive reach, flexibility, and easy exportation. Initiating sales

through established marketplaces serves as a pragmatic approach for early

traction, providing a launch pad for businesses.

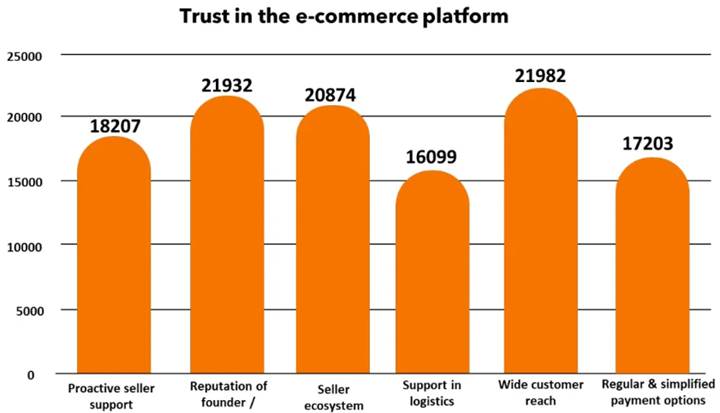

Selecting Platforms

In

the e-commerce landscape, the survey uncovered a wishlist

of factors that are crucial for instilling trust among sellers. Nearly 99% of

respondents, totaling 21,982, expressed a strong preference for platforms with

a wide customer reach, emphasizing the significance of reaching a diverse

audience, followed by the reputation of the founder/marketplace as noted by

21,932 respondents. A robust seller ecosystem was identified as pivotal by

20,874 sellers, highlighting the importance of a collaborative and supportive

community. Proactive seller support, along with the availability of regular and

simplified payment options, and logistical assistance, rounded out the wishlist, showcasing the sellers' desire for comprehensive

and reliable support systems from e-commerce platforms.

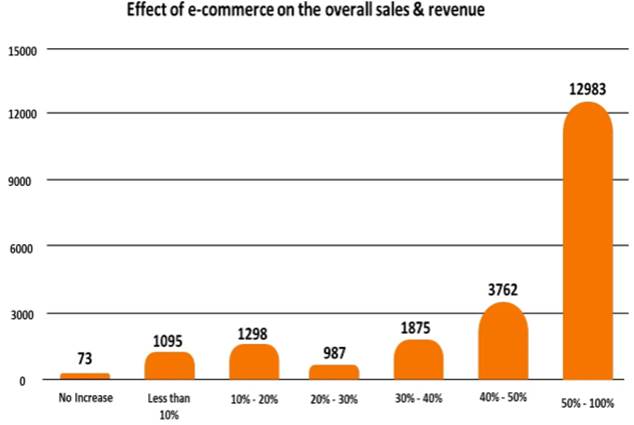

Online Catalyzes Business Growth by 50%

More

than 50% of the respondents, that is 12,983 businesses have had a substantial

boost in sales of more than 50%, with another 3,762 respondents having stated

that they have seen an increase between 40% 50%, whereas 4,160 respondents have

seen an increase between 10% 40%. The ability to tap into a worldwide audience

has proven instrumental in driving substantial sales improvements for a

considerable number of businesses and the importance of worldwide market is

evident in its capacity to offer businesses unparalleled opportunities for

expansion, diversification, and increased competitiveness in the ever-evolving

landscape of global commerce.

On

the other hand, only 1,095 respondents experienced less than a 10% sales

uptick, and a mere 73 reported no overall revenue increase.

The

advent of e-commerce giants like Amazon and Flipkart has notably elevated sales

income, particularly in the D2C sphere. Social commerce in India is poised for

exponential growth, projected to reach US$ 16-20 billion by FY25, driven by an

impressive CAGR of 55-60%.*

*https://www.ibef.org/industry/ecommerce

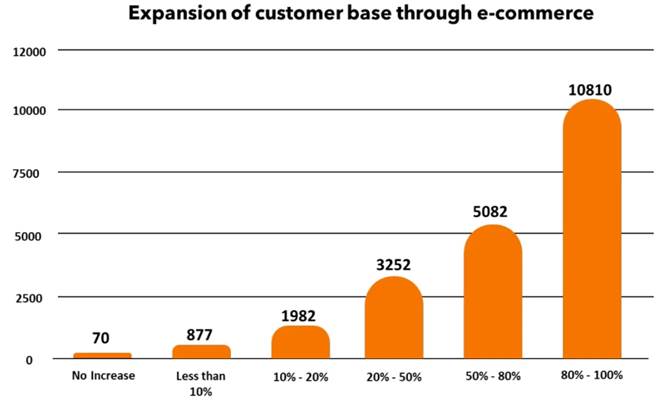

New Customer Acquisition Easier Online

The

survey findings reveal a notable positive impact on customer base expansion

following the adoption of an online presence. A substantial 48.97% of

respondents, totaling 10,810 businesses, reported a remarkable increase of over

80% in their customer base. Additionally, 5,082 respondents noted a significant

growth ranging between 50% to 80%, while 5,234 businesses experienced a

customer base increase ranging from 10% to 50%. Only 877 respondents reported a

modest increase of less than 10%, highlighting the overall positive trend in

customer acquisition through online channels.

In

contrast, a mere 70 respondents expressed no increase in their customer base

despite establishing an online presence. This minority underscores the need for

targeted training and education initiatives to empower these businesses in

leveraging digital platforms effectively.

There

has also been a rise in the customer base on e-commerce platforms as was seen

through the analysis of the India Brand Equity Foundation's e-commerce industry

report 2023 which indicates that in the last three years the online shoppers

have risen by 125 million and this number is expected to further increase by

another 80 million by the year 2025*.

*https://www.ibel.org/industry/ecommerce

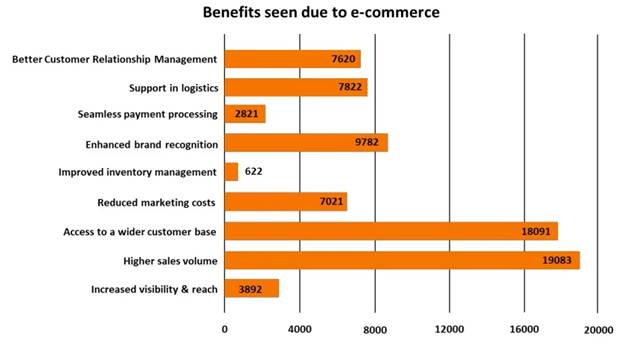

Online Drives Higher Sales & More Customers

The

survey results highlight the substantial positive impact experienced by

businesses selling on e-commerce platforms, particularly in terms of increased

sales volume and access to a broader customer base with high responses at

19,083 & 18,091 respectively. The geographical liberation afforded by these

platforms stands out as a significant driver, with 7,822 responses, enabling

businesses to reach customers far beyond their local regions. Moreover, 9,782

respondents believe that venturing online has significantly improved their

brand recognition, which indicates that the exposure gained through e-commerce

platforms has played a crucial role in increasing the visibility and awareness

of their brands among consumers. Businesses are also succeeding in establishing

a more enhance customer relationship management system with 7,620 responses

being in favor of this positive impact. Another noteworthy finding is that over

7,021 respondents feel that e-commerce has led to a reduction in marketing

costs, indicating that the efficiency and reach of online platforms have

allowed businesses to achieve effective marketing results with lower expenses,

contributing to improved cost-effectiveness.

Additionally,

it is also highlighted that businesses are still facing complications in

retrieving payments and widening their brands visibility. Lastly, the

discrepancy in experience between ease of sales vs ease of post-purchase

fulfillment payments (2,821 responses) is an issue warranting action from

policy makers by way integration of payment settlement platforms and

seller-side fintech innovations to eliminate leakage between digital order

acquisition and realization cycles. The aspect of brand visibility too merits

more discourse. The lower agreement of 3,892 on actual conversions reveals gaps

in brand positioning, communication strategies once buyers land on product

pages. This indicates the scope for further education of sellers on effective

online merchandising. The lowest responses was garnered for improved inventory

management at only 622. Therefore, while validating the directional positive

impact of e-commerce adoption, the survey also flags important nuances

requiring addressing through supportive interventions for sustaining seller

success online.

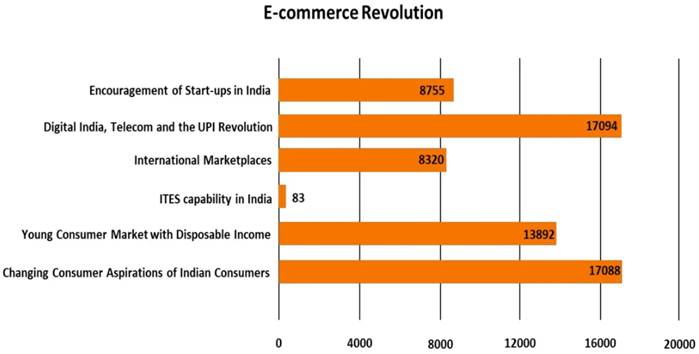

Digital India & UPI Drivers of Transformation in MSMEs

A

substantial majority of respondents, accounting for 17,094, attributed their

motivation to the transformative effects of the Digital India initiative, the

Telecom Revolution, and the widespread adoption of Unified Payments Interface

(UPI). The Digital India program, a catalyst for the escalating prominence of

e-commerce in India, has played a pivotal role in fortifying digital

infrastructure. As of February 2023, this initiative has resulted in an

impressive 1.2 billion telecom subscribers and a staggering 30 billion UPI

transactions within a five-month span, establishing a robust foundation for the

burgeoning growth of e-commerce*.

Furthermore,

a noteworthy segment of respondents, totaling 13,892, stated that they were

amused by the young consumer market with disposable income and 7,088

respondents underscored that their engagement with e-commerce platforms was

spurred by the evolving aspirations of Indian consumers. This signifies a

growing awareness among businesses of the shifting preferences and expectations

of the consumer base, prompting a strategic realignment

towards

the dynamic landscape of online commerce.

One

of the factors leading to a change in consumer aspirations is the rise in

household incomes. It is anticipated that the elites will make up at least a

third of the total consumption by 2025. This will also be coupled in an

increase in urbanization and the rise of nuclear family systems in India which

will all contribute to higher household income**.

Some

other factors that were responsible for sellers to join e-commerce platforms

includes, encouragement of startups in India, accessibility to the

international marketplace and ITES capabilities in India.

*https://www.ey.com/en_in/india-at-100/digitalizing-india-a-force-to-reckon-with

**https://www.bog.com/publications/2017/marketing-sales-globalization-new-indian-changing-consumer

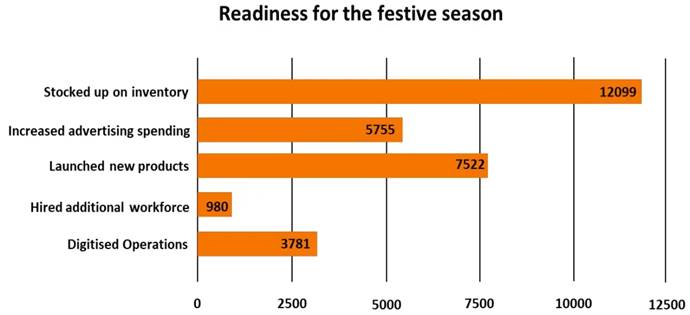

Sellers Rely on Innovation to Attract More Consumers

In

a comprehensive exploration of seller preparedness during the festive season,

the survey reported that the majority, comprising 12,099 respondents,

emphasized the significance of stocking up inventory as a primary measure.

Consumer spending during the festive season increases by about 12% on clothing

and about 14% on recreation, entertainment and leisure. Therefore, businesses

prepare to meet the rise in demand by increasing their stocks*.

In

addition, 7,522 respondents emphasized the strategic introduction of new

products during this specific timeframe. Acknowledging the escalated consumer

demand prevalent during festive seasons, the unveiling of new products not only

addresses this surge in demand but also establishes a competitive edge within

the dynamic market. A 2022 report released by Meta aligns with these insights,

revealing that an impressive 93 percent of consumers express a willingness to

explore new brands and products during festive periods. This observation

underscores the efficacy of product launches as a strategic approach to

fostering business growth during the festive season.

Furthermore,

businesses have undertaken additional preparedness measures to effectively

navigate the festive season. This includes a notable increase in advertising

expenditure, as launching seasonal discount programs across a range of products

serves to attract customers. Additionally, the digitalization of operations has

been implemented to enhance overall efficiency, complemented by the recruitment

of supplementary staff to adeptly manage the seasonal surge in demand. These

comprehensive strategies collectively position businesses to navigate

challenges and capitalize on the myriad opportunities presented during the

festive season.

*https://www2.deloitte.com/in/en/pages/consumer-business/articles/indian-consumers-to-spend-more-on-luxury-this-festival-season.html

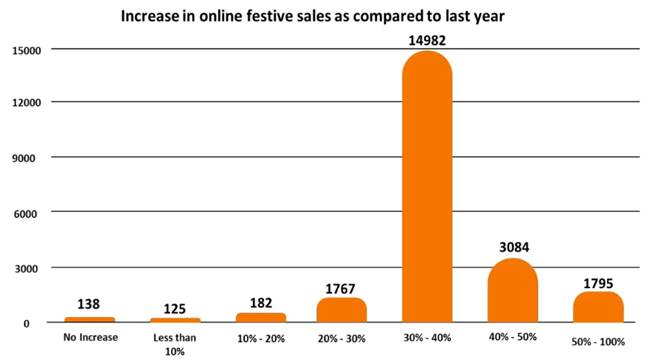

Online Spurs Over 30% YoY Growth

The

festive season brought a substantial surge in online sales for businesses who understood

how to harness the potential of selling online, with an impressive 14,982

respondents experiencing remarkable growth ranging from 30-40%. 4,879

respondents reported an increase in the range of 40-100%, emphasizing the

festive season's pivotal role in propelling sales figures. Additionally, 1,949

respondents experienced growth between 10%-30%, followed by a modest 125

respondents reporting a growth of less than 10%, reflecting varying degrees of

success during the festive season. Lastly, 138 respondents indicated no

increase in online sales compared to the previous year, providing a

comprehensive view of the impact on online sales across different segments.

According

to Unicommerce, E-commerce order volumes grew

handsomely this festive season, increasing by approximately 37% during the

festive season sale of 2023 as compared to the festive sale period in 2022. The

gross merchandise value (GMV) also saw an increase of 22 per cent during the

same festive period. The success of the festive season sales in parts may be

attributed to attracting discounts on the online marketplaces and robust

advertising campaigns. This has helped marketplaces record an impressive year-on-year

(YoY) order volume growth of 39%. Brand websites, on the other hand, also

reported a strong 23% increase in e-commerce order volumes*.

*https://infowordpress.s3.ap-south-1.amazonaws.com/wp-content/uploads/2023/08/14114209/India-Ecommerce-Index-2023.pdf

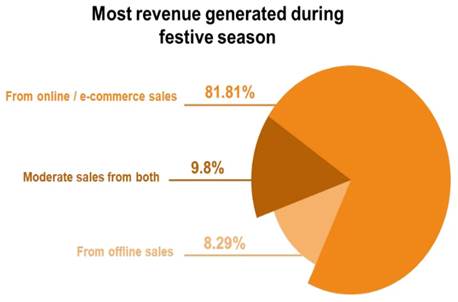

Over 80% MSMEs Generate More Revenues Online

The survey reported a

dominant trend in revenue generation during the festive sales period, with a

substantial 81.81% of respondents attributing the majority of their revenue to

online and e- commerce sales. This underscores the pivotal role of digital platforms

in driving sales and revenue growth for businesses during festive seasons. The

widespread adoption of online channels is evident in the significant majority

favoring this route for revenue generation.

The survey reported a

dominant trend in revenue generation during the festive sales period, with a

substantial 81.81% of respondents attributing the majority of their revenue to

online and e- commerce sales. This underscores the pivotal role of digital platforms

in driving sales and revenue growth for businesses during festive seasons. The

widespread adoption of online channels is evident in the significant majority

favoring this route for revenue generation.

In

contrast, 9.8% of respondents reported sales from both online & offline

channels and the remaining 8.29% of the respondents noted that they received

the most revenue for their products from offline sales during the festive

season. While a minority, this group emphasizes the continued relevance of

offline sales channels for certain businesses, highlighting the importance of

maintaining a diversified sales strategy to cater to varying consumer

preferences and market dynamics.

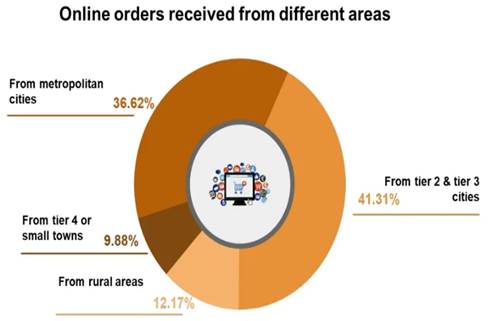

Consumers in Tier 2, 3, 4 & Rural Areas Drive MSME Orders

Online

The survey's analysis of online

and e-commerce sales order traffic reveals intriguing patterns in the

geographical distribution of consumer engagement. In a significant shift, the

majority of respondents that is 41.31% identified Tier 2 and Tier 3 cities as

the primary source of their online order traffic. This trend reflects the

expanding influence and increasing online participation of consumers in smaller

urban centers. As these cities embrace e-commerce, businesses targeting these

areas are poised to benefit from the growing trend and capitalize on the

evolving consumer behavior. In major urban centers, specifically metropolitan

cities, a notable 36.62% of respondents reported the highest order traffic.

The survey's analysis of online

and e-commerce sales order traffic reveals intriguing patterns in the

geographical distribution of consumer engagement. In a significant shift, the

majority of respondents that is 41.31% identified Tier 2 and Tier 3 cities as

the primary source of their online order traffic. This trend reflects the

expanding influence and increasing online participation of consumers in smaller

urban centers. As these cities embrace e-commerce, businesses targeting these

areas are poised to benefit from the growing trend and capitalize on the

evolving consumer behavior. In major urban centers, specifically metropolitan

cities, a notable 36.62% of respondents reported the highest order traffic.

The

data also highlights the presence of online shopping in tier 4, small towns and

rural areas with 22.05% of respondents reporting the highest order traffic from

such regions. This suggests a growing acceptance of digital transactions beyond

urban boundaries, presenting businesses with opportunities to cater to

previously underserved markets.

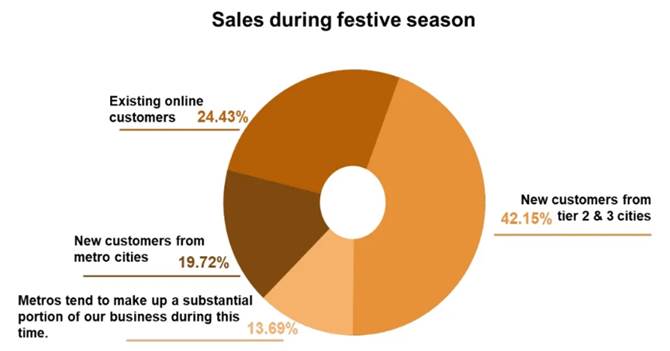

Tier 2 & 3 Cities Drive Customer Growth

Businesses

navigating the festive season landscape must strategically balance their

engagement with existing customers and the pursuit of new customer segments,

especially in emerging urban markets. Geographically, Tier 2 and Tier 3 cities

took center stage, outpacing metros in order traffic and signaling a

significant shift in consumer behavior.

The

majority of respondents that is 42.15% identified new customers from Tier 2 and

Tier 3 cities as the primary source of their festive season orders, which

underscores the expanding footprint of businesses into smaller urban centers

during festive periods, highlighting the growing interest and participation of

consumers in these areas in the online shopping experience. 24.43% of

respondents observed that the bulk of their festive season orders stemmed from

loyal existing online customers, showcasing the enduring impact of customer

retention efforts.

Moreover, 19.72% of respondents reported a significant contribution from new customers in metro cities, affirming the ongoing relevance of major urban centers in festive season sales. Only 13.69% of respondents expressed that metros tend to constitute a substantial portion of their business during the festive season.

Rising

disposable incomes owing to economic growth in smaller urban centers, has

created an aspirational consumer base of youth from Tier 2 & 3 cities. For

these youth, buying branded or trendy products online is seen as a reflection

of their modern outlook and a way of keeping up with their urban peers. Festive

occasions loosen budgets further for such purchases and the heavy discounts and

deals offered during festive sales provide further incentives for them to

indulge in online shopping. Emulating urban consumption habits also drives

small town youth who are more open to shopping online versus older consumers.

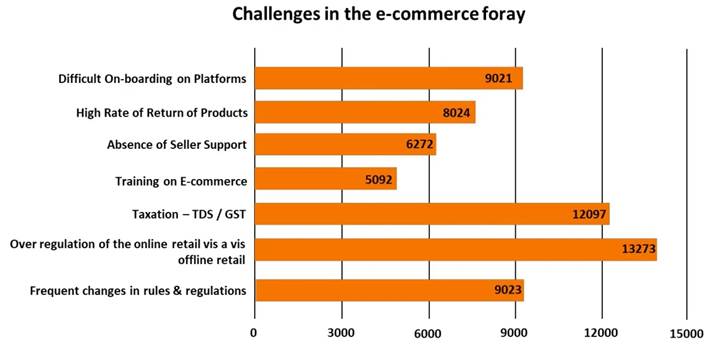

Overregulation of Online Retail Cited as Major Challenge

A

predominant challenge highlighted by a majority that is 13,273 respondents in

the e-commerce sector revolves around the issue of over-regulation in online

retail. This indicates perceived gaps in policy frameworks governing e-commerce

platforms versus brick-and-mortar stores, posing divergent compliance burdens

between online and offline sellers could disadvantage e- commerce businesses.

The overregulation of e-commerce compared to traditional retail creates an

unequal regulatory burden for online sellers. Additionally, 12,097 respondents

emphasized that taxation poses a significant hurdle for numerous e-commerce

sellers, citing the complex nature of tax norms for online selling.

Further

challenges identified by respondents include difficulties in onboarding

platforms, a high rate of product returns, absence of robust seller support,

training requirements, and the impact of frequent changes in rules and

regulations. These collective challenges underscore the multifaceted landscape

that businesses in the e-commerce domain navigate, necessitating a strategic

approach to address regulatory, tax, and operational complexities.

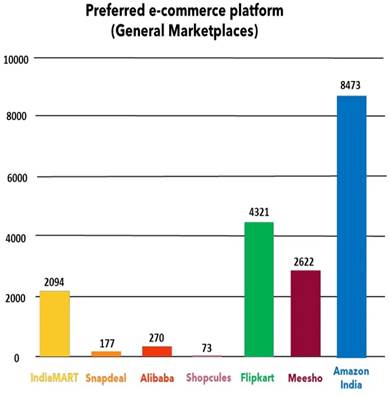

E-commerce Platforms

The

survey further reported the most favored platform preference of the respondents

in four different categories. From the available general marketplace of

e-commerce platforms, Amazon emerged as the most favored choice, followed by

Flipkart, Meesho, IndiaMart,

Alibaba, Snapdeal, and Shopclues. Amazon's prominence

in this category can be attributed to its extensive global reach, offering

sellers a multitude of benefits such as valuable insights, efficient inventory

facilities, a broad market reach, and robust marketing tools. These factors

collectively position Amazon as a highly favorable platform for sellers seeking

a versatile and impactful online marketplace.

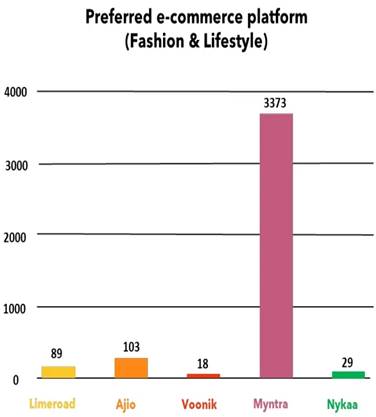

In

the realm of fashion and lifestyle e- commerce, Myntra emerged as the top

choice among respondents, followed by Ajio, Limeroad,

Nykaa, and Voonik. Myntra's

popularity in this category is attributed to its status as a major fashion and

lifestyle hub, offering a diverse range of products and brands. The platform's

extensive variety and brand offerings make it a preferred choice for sellers

operating in the fashion and lifestyle sector, seeking a prominent and

versatile platform to showcase and sell their products.

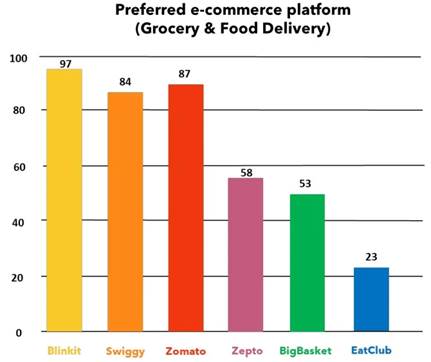

E-commerce Platforms

The notable trend in the

realm of grocery & food delivery services, Blinkit

emerged as the most favored platform,

surpassing competitors such as Swiggy, Zomato, Big Basket, Zepto,

and Eat Club. This preference for Blinkit is

attributed to its reputation for swift deliveries, particularly through

collaborations with local stores. Positioned as the largest e- grocery platform

in India, Blinkit has gained widespread popularity,

making it the preferred choice for fulfilling diverse grocery and household

requirements.

The notable trend in the

realm of grocery & food delivery services, Blinkit

emerged as the most favored platform,

surpassing competitors such as Swiggy, Zomato, Big Basket, Zepto,

and Eat Club. This preference for Blinkit is

attributed to its reputation for swift deliveries, particularly through

collaborations with local stores. Positioned as the largest e- grocery platform

in India, Blinkit has gained widespread popularity,

making it the preferred choice for fulfilling diverse grocery and household

requirements.

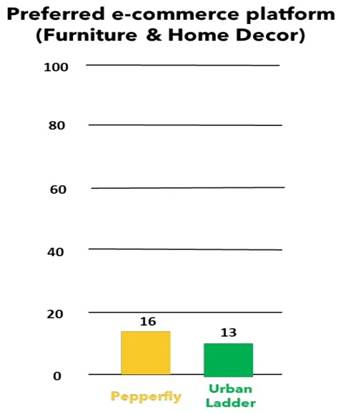

Pepperfry was identified as the preferred choice for

furniture and home decor, followed by Urban Ladder. Pepperfry

has solidified its position as the leading e- commerce platform for furniture,

making it a favorable and prominent choice for sellers operating in the

furniture and home decor industry.

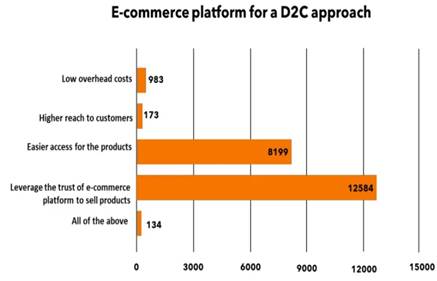

D2C Model- Key for MSME Growth

A predominant share of

survey respondents reported multiple factors contributing to the suitability of

e-commerce as a Direct-to- Consumer (D2C) approach. Key considerations include

leveraging the trust associated with e-commerce platforms for effective product

sales, streamlined access to products, and an extensive reach to potential

customers. D2C businesses express confidence in the reliability of e- commerce

channels, emphasizing the ease with which potential buyers can access their

15000 products and the broad customer reach facilitated by these platforms. In

contrast, a minority of 134 respondents favors the traditional offline

marketing approach.

A predominant share of

survey respondents reported multiple factors contributing to the suitability of

e-commerce as a Direct-to- Consumer (D2C) approach. Key considerations include

leveraging the trust associated with e-commerce platforms for effective product

sales, streamlined access to products, and an extensive reach to potential

customers. D2C businesses express confidence in the reliability of e- commerce

channels, emphasizing the ease with which potential buyers can access their

15000 products and the broad customer reach facilitated by these platforms. In

contrast, a minority of 134 respondents favors the traditional offline

marketing approach.

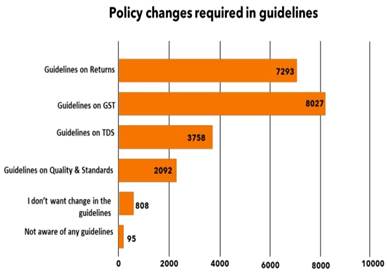

A sizeable

portion of respondents that is 8,027, highlighted the need for revisions in

guidelines pertaining to GST. This indicates that the current norms around

these aspects pose certain challenges. Under current GST norms, traditional

businesses with less than Rs. 40 lakh turmover are

exempt from obtaining GST registration. However, on e-commerce platforms, there

is no such exemption. Even sellers with very modest turnover are mandated to

have GST registration to enable inter-state sales.

A sizeable

portion of respondents that is 8,027, highlighted the need for revisions in

guidelines pertaining to GST. This indicates that the current norms around

these aspects pose certain challenges. Under current GST norms, traditional

businesses with less than Rs. 40 lakh turmover are

exempt from obtaining GST registration. However, on e-commerce platforms, there

is no such exemption. Even sellers with very modest turnover are mandated to

have GST registration to enable inter-state sales.

Moreover,

innovative promotion avenues through influencer marketing is a game changer for

D2C brands but despite all of this, Micro-entrepreneurs have to navigate

complex GST registration, filing processes diverting bandwidth from core

operations. Additionally, 7,293 respondents express the need for changes in

return guidelines, emphasizing the financial burden imposed by expensive retum processes. Streamlining return filing periodicity,

introducing automated reconciliations, and provisions for amendment can improve

compliance.

Another

concern highlighted by 3,758 respondents pertains to the complexity of Tax

Deducted at Source (TDS) guidelines, suggesting a desire for clarity and

simplification in this area due to need of rationalization to avoid unwarranted

tax burdens. Suitable changes in TDS applicability and payment can prevent

locked up capital for the sector. Moreover, 2,092 respondents have expressed

the need for changes in Guidelines on Quality & Standards. Clearer

guidelines on safety, reliability, and performance metrics tailored for

e-commerce would help ensure quality consistency, enable self-compliance, and

protect consumer interests. Updated standards would encourage voluntary

adherence and cultivate customer trust in the e-commerce ecosystem. Meanwhile,

a notable 808 respondents expressed contentment with the current guidelines and

prefer no changes. These insights shed light on the multifaceted challenges

businesses face.

Way

Forward

As

economies increasingly digitalize, MSMEs will need to adopt digital solutions

to compete and thrive. Enterprises that are not connected with e-commerce

platforms are likely to face greater difficulty in accessing markets at a time

when integrated enterprises are making deeper inroads into markets with the use

of platforms. Given that integrated firms perform better on average than

non-integrated enterprises, inequalities in market access caused by e-commerce

platforms can accentuate imbalances between these firms. The e-commerce

industry has emerged as a catalyst for the transformative growth of Micro,

Small, and Medium Enterprises (MSMEs) in India, fostering development through

funding, technology infusion, and targeted training initiatives. This positive

influence has not only empowered local businesses but has also triggered a

ripple effect in adjacent industries. As India's e-commerce sector propels

towards becoming the world's second-largest market by 2034 by overtaking the

United States, rapid expansions and technological innovations such as digital

payments, hyper- local logistics, analytics-driven customer engagement, and

digital advertising are anticipated to be pivotal contributors to its

burgeoning success*.

The

trajectory of the Indian e-retail business is marked by ambitious projections,

with expectations of engaging 300-350 million shoppers over the next five

years. The online Gross Merchandise Value (GMV) is poised to surge to US$

100-120 billion by 2025, according to a comprehensive report by the Indian

Brand Equity Foundation. Recognizing the potential embedded in this growth,

MSMEs are encouraged to leverage initiatives led by prominent platforms like

Amazon and Flipkart, strategically enrolling small sellers to bolster their

e-commerce presence. Governmental efforts to fortify the e-commerce landscape

for small businesses should be prioritized, particularly during festive

seasons, where these enterprises showcase their resilience and prosperity in

the online realm. However, challenges such as complex taxation policies,

intricate return procedures, delayed payments, and obscured fees on major

e-commerce platforms necessitate meticulous attention. Addressing these issues

through equitable contracting and robust dispute resolution mechanisms is

imperative for fostering a conducive environment. Simultaneously, enhancing

cyber security readiness is paramount to safeguard the interests of businesses

operating in the digital sphere. As India's SMEs demonstrate their prowess in

thriving during the festive season, the e-commerce wave presents a remarkable

opportunity for reaching new customers and steering post-pandemic growth.

Collaborations, supportive policies, and proactive preparedness will be

instrumental in harnessing the potential of e-commerce as a game- changer for

small and medium-sized businesses in India. Furthermore, the platform's

experiencing a surge in festive exports from India underscores the global

appeal of Indian products. Top export categories, including artificial jewelry,

cosmetics, grooming essentials, clothing, and accessories, exemplify the

diverse offerings driving demand in key markets such as the United States, the

United Kingdom, Germany, Australia, Canada, France, and the United Arab Emirates.

This international demand underlines the platform's role in connecting Indian

sellers with a global audience and contributing to the global prominence ofIndian goods during celebratory occasions.

*https://www.ibel.org/industry/ecommerce

India

SME Forum, the voice of MSMEs in India, has taken the lead in forming the Forum

for Internet Retailers, Sellers & Traders, (FIRST India) in order to

support the entry of retailers, sellers and traders who have been inducted in

the definition of micro, small and medium enterprises under the MSMED Act 2006

on the advice of the Advisory Committee constituted under subsection (2) of

section 7 of the MSMED Act 2006.

The

Indian retail, trade & commerce sector, representing enterprises based in

India, which are in the business of wholesale & retail selling of goods and

services, both, offline as well as online to consumers, are all eligible under

this change notified on 2nd July 2021.

India

SME Forum has pushed for the inclusion of wholesale and retail trade, as

activities eligible under the MSMED Act with benefits restricted to priority

sector lending, as of now.

Together

with Indian policymakers, FIRST India represents over 70,000 traders, merchants

and resellers and is committed to help create a conducive policy and ecosystem

which will help remove, the biggest obstacles for online merchants to expand

their business nationally as well as across-borders.

More

information on: www.1stindia.org

Delhi:

DD-30, Second Floor, Nehru

Enclave, Kalkaji, New Delhi-110019

Mumbai:

404, Durga Chambers, Veera Indl.

Estate, Veera Desai Andheri (w),

Mumbai- 400053,

India